November 2016

THE MONTH IN BRIEF

Bulls were reined in during October. The S&P 500 lost 1.94% as Wall Street responded unenthusiastically to the fall earnings season. Even though much of the economic news that emerged in October was good, investors saw an interest rate hike on the horizon and remained concerned about an increasingly controversial presidential race. Consumer confidence waned, but improved manufacturing, consumer spending, and retail sales numbers all factored into stronger growth. New and existing home sales accelerated. The price of oil rose, then quickly fell; the price of gold slipped, then recovered just a bit. Overseas, a timeline was set for the Brexit. In the big picture, appetite for risk waned as investors remained cautious.

DOMESTIC ECONOMIC HEALTH

Economic indicators flashed clear signals that the economy was picking up. Household spending rose a healthy 0.5% during September, the most since June. Household incomes rose 0.3% in the ninth month of the year. Retail sales were up 0.6% for September, with core retail purchases rising 0.5%.

Important twin gauges of business activity showed both manufacturing and service sector growth. The Institute for Supply Management’s non-manufacturing purchasing manager index jumped up to a reading of 57.1 in September, improving 5.7 points. ISM’s factory PMI also recovered from an August spent in contraction territory, rising 2.1 points to 51.5 in September; even more encouragingly, ISM’s new factory orders index increased by 6.0 points.

Complementing all this, the federal government said that the economy grew 2.9% in the third quarter – a real upturn from the 1.4% GDP recorded for Q2.

Had full employment been reached? Perhaps it was close at hand, since the hiring pace seemed to be moderating. The Department of Labor said that companies had added 156,000 net new jobs in September, while revising the August gain north to 167,000. The jobless rate rose slightly to 5.0%; the U-6 rate including the underemployed remained at 9.7%. Average hourly wages improved another 0.2%.

Was inflation pressure mounting? Not really. The PCE price index advanced 0.2% in September, which left the core PCE index up 1.7% year-over-year, the same as in August. The Consumer Price Index showed a 1.5% annual gain in September, up from 1.1% a month earlier; core consumer prices were up 2.2% in 12 months, ticking down from 2.3% in August. Producer prices rose 0.3% in September, but that still left them up just 0.7% year-over-year.

Some indicators did descend, most notably those measuring consumer confidence. The Conference Board’s monthly barometer dipped 4.9 points in October to a respectable 98.6 mark, while the University of Michigan consumer sentiment index fell to 87.2 at month’s end. Headline capital goods orders also declined 0.1% for September, with core orders down 1.2%.

GLOBAL ECONOMIC HEALTH

In London, United Kingdom prime minister Theresa May announced definite plans for the Brexit. The U.K. will invoke Article 50 of the Lisbon Treaty no later than the end of March 2017. Assuming this occurs, the U.K. will leave the European Union in the summer of 2019. Until then, it intends to remain a player in all E.U. summits and member state negotiations. Speaking of the broader E.U., Eurostat reported economic growth of 0.3% for the euro area in Q3 and estimated annualized inflation for the euro area at 0.5% in October.

The World Bank projected 6.7% growth for China in 2016, declining to 6.5% in 2017, and then 6.3% in 2018. It believes that the second-fastest growing economy in Asia this year will be that of the Philippines at 6.4%. Malaysia’s 2016 GDP is projected at 4.2%; Indonesia’s, at 4.8%. China aside, the Bank expects growth to pick up across Asia in the near future, projecting 4.8% growth for the rest of the region’s economies this year, 5% GDP in 2017, and 5.1% growth for 2018. Meanwhile, news arrived that Japan’s retail sales and industrial output were flat in September; retail sales were down for a seventh straight month and 1.9% lower over the past 12 months.

WORLD MARKETS

Many foreign indices outperformed ours. To our respective north and south, the TSX Composite advanced 0.42% last month; the Bolsa, 1.62%. Argentina’s MERVAL rose 7.16%. European indices had a good month – there were gains of 1.47% for the DAX, 1.37% for the CAC-40, 4.81% for the IBEX 35, 0.59% for the Micex, and 0.80% for the FTSE 100. The FTSEurofirst 300 was an exception, losing 0.90%.

The Nikkei 225 soared 5.93% during October to pace the major Asian indices. The Shanghai Composite was not that far behind, rising 3.22%. October also brought gains of 0.66% for India’s Sensex and 2.49% for the FTSE Taiwan 50. Australia’s All Ordinaries retreated 2.22%, and Hong Kong’s Hang Seng, 1.56%. The MSCI World index lost 2.01%, but the MCSI Emerging Market index rose 0.18%.

COMMODITIES MARKETS

As the Halloween trading day drew to a close on Wall Street, a look at the COMEX and NYMEX showed monthly losses for both gold and oil. The yellow metal slipped 3.27% for the month, settling at $1,276.70. Light sweet crude dropped to $46.76 at month’s end with oil investors still awaiting finalization of OPEC’s deal to restrain output; futures took a 2.68% fall for October.

Reviewing the performance of other commodities last month, we see solid gains for some key crops. Coffee rose 9.25%; corn, 5.80%; cotton, 4.02%; soybeans, 5.30%; and wheat, 2.86%. Cocoa lost 0.90% in October; sugar, 2.09%. Among metals, silver slipped 7.09%; platinum fell 4.71%; and copper, 0.11%. Silver finished the month at $17.84. Unleaded gasoline futures lost 4.66% in October; heating oil futures, 1.62%. Natural gas futures gained 3.65%. The U.S. Dollar Index settled at 98.32, rising 3.03% in a month.

REAL ESTATE

Aside from a drop in groundbreaking, the news out of this sector was decidedly upbeat. New home sales rose 3.1% in the ninth month of 2016, taking the 12-month advance to 29.8% and leaving the pace once again near a 9-year high. Meanwhile, the National Association of Realtors noted a 3.2% monthly advance for existing home sales.

Home prices – as measured by the 20-city S&P/Case-Shiller index – were up 5.3% year-over-year as of August, compared with 5.0% in the year ending in July. The Census Bureau said that building permits increased 6.3% for September; though, housing starts did retreat 9.0%. Pending home sales were up 1.5% for September according to NAR.

Mortgages grew more expensive last month. By October 27, the mean interest rate for the 30-year FRM was at 3.47%, according to Freddie Mac’s Primary Mortgage Market Survey, while average rates on the 15-year FRM and the 5/1-year ARM respectively stood at 2.78% and 2.84%. Back on September 29, the mean rate on the 30-year loan averaged 3.42%; the average interest on the 15-year fixed was 2.72%; and the mean interest on the 5/1-year adjustable rate mortgage was 2.81%.

LOOKING BACK…LOOKING FORWARD

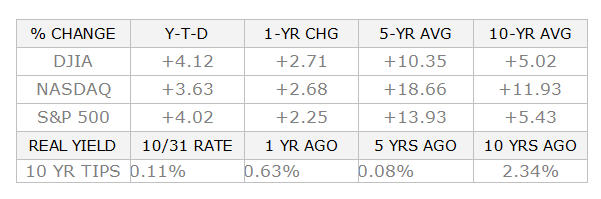

All three major U.S. equity indices lost ground in October. The blue chips retreated least – the Dow Jones Industrial Average gave back 0.90% for the month. Dropping 2.31%, the Nasdaq Composite exceeded the S&P 500’s 1.94% loss. The Russell 2000 stumbled 5.42%. Unsurprisingly, considering all this, the CBOE VIX soared 29.42% with uncertainty rising on Wall Street. The Halloween settlements: DJIA, 18,142.12; NASDAQ, 5,189.13; S&P, 2,126.15; RUT, 1,191.39; and VIX, 17.06. The VIX outgained all consequential U.S. indices last month by a wide margin; the PHLX Utility Index logged the biggest advance among the equity indices for October, rising 1.12%.

Sources: barchart.com, bigcharts.com, treasury.gov – 10/31/16

Indices are unmanaged, do not incur fees or expenses, and cannot be invested into directly. These returns do not include dividends. 10-year TIPS real yield = projected return at maturity given expected inflation.

At this writing, it seems highly unlikely that the Federal Reserve will authorize an interest rate hike at the start of November, as the Federal Open Market Committee has historically preferred to refrain from any policy decisions that could influence presidential elections. According to FactSet data, year-over-year earnings growth is apparent for the first time since Q1 2015 (blended Q3 earnings growth was at 1.6% through Halloween). Still, there is nothing resembling a bull run as we enter November. Hopefully, some risk appetite will return after the election, and investors will view solid economic indicators as validations of an improving economy, first, and as further evidence for a federal funds rate increase, second. Wall Street could see a lot of volatility this month, not merely reflective of the election. We can only hope the evident tension among institutional investors eases and the market surprises to the upside.

UPCOMING ECONOMIC RELEASES: After the Federal Reserve policy statement on November 2, the rest of the major items on the economic release slate arrives in this order: the ISM October non-manufacturing PMI; September factory orders and the October Challenger job-cut report (11/3); the Department of Labor’s October employment report (11/4); September consumer credit (11/7); the preliminary November consumer sentiment index from the University of Michigan (11/11); October retail sales (11/15); the October PPI and October industrial output (11/16); the October CPI and October housing starts and building permits (11/17); October existing home sales (11/22); the final November University of Michigan consumer sentiment index, October new home sales, October capital goods orders, and the minutes from the November Federal Reserve policy meeting (11/24); the newest consumer confidence index from the Conference Board, the September S&P/Case-Shiller home price index, and the second estimate of Q3 growth (11/29); and then the November ADP payrolls report, a new Federal Reserve Beige Book, and October PCE prices, consumer spending, and pending home sales (11/30).

Securities offered through 1st Global Capital Corp., Member FINRA/SIPC. Investment advisory services including fee-based asset management accounts held through NFS, LLC are offered through 1st Global Advisors, Inc. All other financial planning and fixed insurance services are offered through Mueller Financial Services, Inc. Mueller Financial Services, Inc. and 1st Global Capital Corp are unaffiliated entities.