The alternative minimum tax (AMT) was enacted back in 1969 to ensure that high-income individuals don’t take advantage of multiple tax breaks and avoid paying federal tax. However, in recent years, the AMT has been imposed on many middle-income taxpayers.

Unfortunately, the Tax Cuts and Jobs Act (TCJA) retains the individual AMT. But AMT exemptions and phaseout thresholds have been increased for 2018 through 2025.

How it works: The AMT calculation runs side-by-side with your regular income tax calculation. The starting point for the AMT is your taxable income calculated under the regular tax rules. Next, you add in “tax preference items” and make other adjustments that disallow some regular tax breaks or change the timing of when they’re taken into account. Then you subtract an AMT exemption amount that’s based on your tax return filing status. The result is your AMT income.

Finally, you apply the AMT tax rates of 26% and 28% to your AMT income and compare the result to your regular tax liability. In effect, you’re required to pay the higher of the two amounts.

Many people are unsure how the changes in the TCJA will affect their specific tax situations. Here are some examples to help you better understand the effects of how the AMT works under the new law. (For simplicity, we’ve assumed all of these imaginary taxpayers are empty nesters who don’t qualify for education-related tax credits or child tax credits.)

The Adams

It’s scary to think that taxpayers with less than $100,000 of taxable income could be hit with the AMT, but that’s just what happened to the Adams family in 2017. Fortunately, the TCJA brings good news: The Adams won’t owe AMT (assuming the same facts) for 2018 under the new law. Here’s why.

In 2017, this married joint-filing couple exercised an “in-the-money” incentive stock option (ISO) granted by the husband’s employer. The difference between the exercise price of the ISO shares and the trading price on the exercise date (the bargain element) was $50,000.

The bargain element doesn’t count as income under the regular tax rules, but it does count as income under the AMT rules.

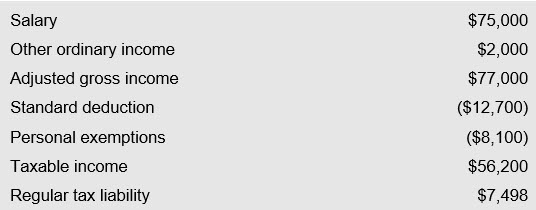

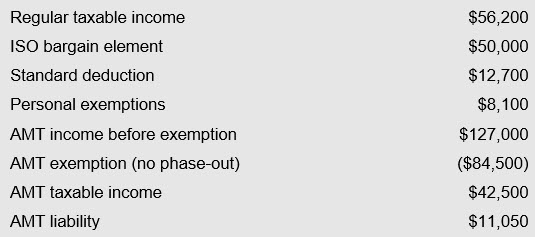

The calculation of the couple’s 2017 regular tax and AMT liabilities are as follows:

2017 Regular Tax Calculation

2017 AMT Calculation

So, for 2017, the Adams family owes $11,050 for the AMT.

Important note: This calculation would have been more complicated if the couple itemized deductions. But, for simplicity, we’ve assumed that they took the standard deduction instead.

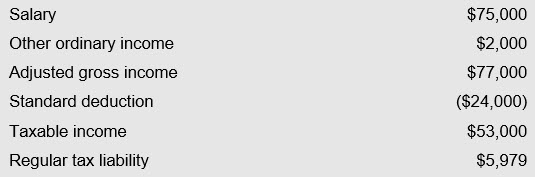

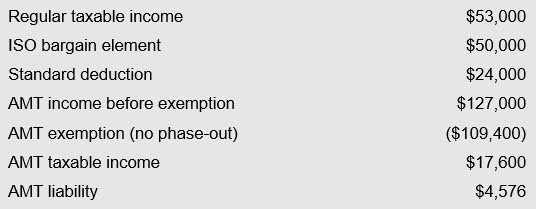

Now, let’s assume the same facts for 2018. The calculation of the couple’s 2018 regular tax and AMT amounts under the TCJA are as follows:

2018 Regular Tax Calculation

2018 AMT Calculation

Thanks to the TCJA, the Adams will not owe AMT in 2018. They’ll owe the regular tax amount of $5,979. So, the new law benefits this couple.

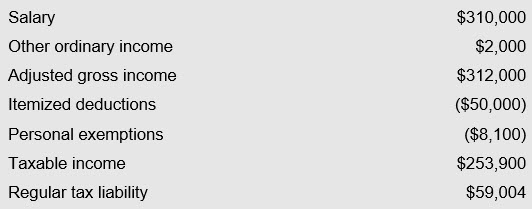

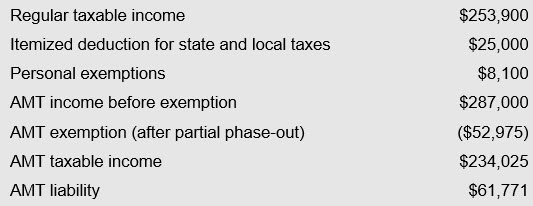

The Bradys

Like the Adams, the Bradys experience a bunch of good luck under the TCJA. That is, they’ll owe AMT under the old rules but not new rules. Here’s how their tax situation will improve from 2017 to 2018.

In 2017, this married joint-filing couple had itemized deductions totaling $50,000, including $25,000 for state and local taxes. The calculation of the couple’s 2017 regular tax and AMT liabilities are as follows:

2017 Regular Tax Calculation

AMT Calculation

For 2017, the Bradys owe the AMT amount of $61,771.

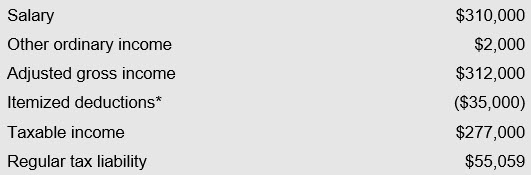

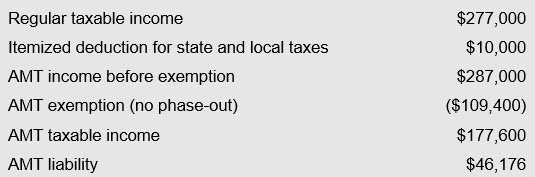

Now assume the same facts for 2018. The calculation of the couple’s 2018 regular tax and AMT amounts under the TCJA are as follows:

2018 Regular Tax Calculation

*For 2018 through 2025, itemized deductions for state and local income and property taxes are limited to $10,000 (combined).

*For 2018 through 2025, itemized deductions for state and local income and property taxes are limited to $10,000 (combined).

2018 AMT Calculation

Thanks to the TCJA, the Bradys won’t be hit with the AMT for 2018. They’ll just owe the regular tax amount of $55,059. So the new tax law benefits this couple.

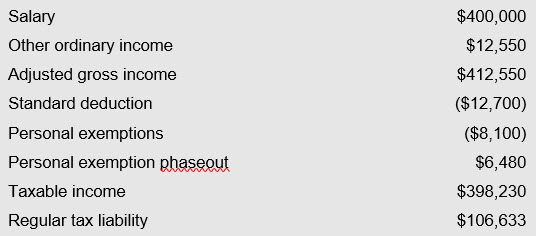

The Cunninghams

Tax Day is never a happy day in the Cunningham house. This is the wealthiest hypothetical couple in our examples. So, it’s not surprising that they’ll owe AMT under both the old and new rules.

In 2017, this married joint-filing couple exercised an in-the-money ISO granted by the wife’s employer. The difference between the exercise price of the ISO shares and the trading price on the exercise date (the bargain element) was $50,000. The calculation of the couple’s 2017 regular tax and AMT liabilities are as follows:

2017 Regular Tax Calculation

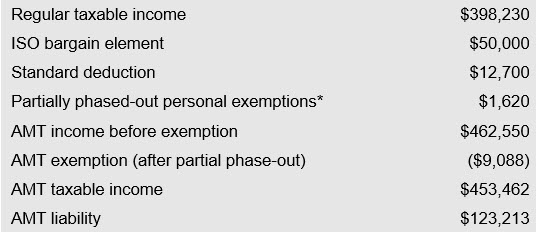

2017 AMT Calculation

* The personal exemption less the phaseout ($8,100 – $6,480).

So, the Cunninghams owe $123,213 in AMT for 2017.

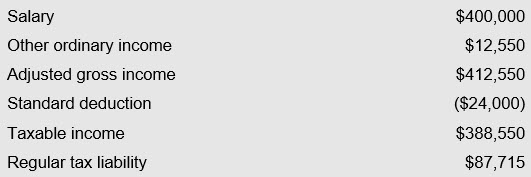

Assuming the same facts for 2018, the calculation of 2018 regular tax and AMT amounts under the TCJA are as follows:

2018 Regular Tax Calculation

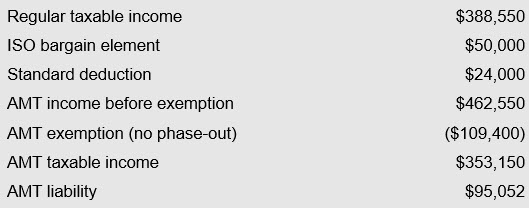

2018 AMT Calculation

In 2018, this couple is still in the AMT zone and owes $95,052 under the AMT rules. However, there is something for the Cunninghams to be happy about: Their 2018 AMT bill is much lower than their 2017 AMT bill, because the increased AMT exemption for 2018 is fully deductible. Therefore, the new law greatly benefits them, even though they still owe the AMT.

Applying Fiction in the Real World

These fictitious examples showcase how the AMT rules have changed for 2018 through 2025 under the TCJA. Although fewer taxpayers will be hit by this dreaded tax under the new law, it still will create headaches for some taxpayers. Consult your tax advisor to discuss customized strategies for minimizing the AMT.

Copyright 2018