With a so-called “stretch IRA,” you build up money in a traditional or Roth IRA during your lifetime. Then, after you die, a younger beneficiary can opt to keep the inherited account open for as long as possible and continues to reap the tax-related benefits.

Unfortunately, the stretch-IRA strategy has lost much of its tax-saving potency due to an unfavorable change included in the new Setting Every Community Up for Retirement Enhancement (SECURE) Act. The law essentially establishes a new 10-year account liquidation rule for most non-spouse beneficiaries who inherit accounts from original account owners. This change is generally effective for accounts inherited by non-spouse beneficiaries from original account owners who die after 2019.

Important: An IRA that was inherited by a non-spouse beneficiary from an original account owner (the person for whom the account was first established) who died before 2020 is unaffected and can still work as a stretch IRA, as under prior law.

But there are alternatives to using stretch IRAs as a wealth-transfer tool. The following six ideas can help you maximize what you leave behind for your heirs and minimize the estate tax hit when you die.

1. Set Up a Roth IRA

Roth IRAs left to non-spouse beneficiaries can still earn federal-income-tax-free income and gains for as long as the account owner lives and for at least 10 years thereafter. Roth IRAs also offer two big advantages over the traditional IRAs as a tax-favored wealth transfer vehicle.

The first is that qualified withdrawals from a Roth IRA are free from federal income tax. The account owner or beneficiary will never owe taxes on qualified Roth IRA withdrawals. Qualified withdrawals are taken after 1) the original account owner has reached age 59½, died or become disabled, and 2) the original account owner has had at least one Roth IRA established in his or her name open for more than five years.

The second advantage is that required minimum distribution (RMD) rules don’t apply for as long as the original account owner is alive. The original Roth IRA owner isn’t required to take any RMDs from the account during his or her lifetime.

If you leave your Roth IRA to your surviving spouse, he or she can retitle the account and treat it as his or her own Roth IRA. Your spouse doesn’t need to take any RMDs for as long as he or she lives. However, when a non-spouse beneficiary (such as your child or grandchild) inherits your Roth IRA, the beneficiary generally must liquidate the account within 10 years after the death of the original account owner. While this rule is unfavorable compared to what was allowed before the SECURE Act, many non-spouse beneficiaries will want to liquidate inherited Roth IRA balances within 10 years anyway. So, the 10-year liquidation rule may not always be viewed unfavorably by heirs.

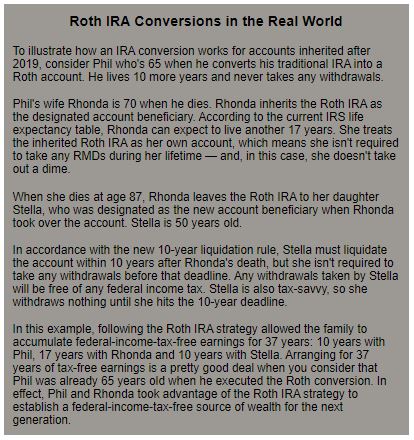

The quickest way to get a substantial amount of money into a Roth account is by converting an existing traditional IRA into a Roth IRA. (See “Roth IRA Conversions in the Real World” below.) Of course, the tax law charges a “price” for using the conversion strategy. Specifically, a Roth conversion is treated as a taxable distribution from your traditional IRA.

Because you’re deemed to receive a taxable cash payout from the converted traditional IRA, the conversion triggers income taxes. In most cases, however, this negative factor is outweighed by several factors.

- The conversion can position you to use the new Roth IRA as a tax-smart wealth transfer vehicle.

- You may be able to reduce the income tax cost of converting a large traditional IRA (say one worth several hundred thousand dollars) by spreading the conversion process over several years. Given today’s relatively low tax rates, it’s a good time to start this process.

- By paying the conversion tax bill today, you’re effectively prepaying future income taxes for the Roth account beneficiary. So, the beneficiary can reap federal-income-tax-free earnings in the future.

2. Make Outright Gifts to Loved Ones

If Roth IRA conversions seem too complicated, consider other tried-and-true estate planning vehicles — such as gifts. Every year, you can give gifts of cash and other assets worth the annual gift tax exclusion to your friends and relatives. For 2020, you (and your spouse) can gift up to $15,000 to as many individuals as you wish without any adverse federal tax effects.

Over time, making these so-called “annual exclusion gifts” can substantially reduce the value of your taxable estate — especially if you give away appreciating assets, such as real estate, stocks and shares of equity mutual funds. You can also make gifts that exceed the $15,000 annual exclusion amount. You won’t owe any gift tax on these “excess gifts” until they surpass the lifetime gift tax exemption. (See “Estate Planning Basics” at right.)

3. Donate to Charities

You can also reduce the value of your taxable estate by transferring assets to tax-exempt charities via charitable gifts while you’re still alive, and via charitable bequests pursuant to a will or living trust arrangement after you pass away. These strategies are especially important for single people who can’t benefit from estate-planning strategies that are available to married couples.

4. Make Gifts to Section 529 Accounts

Section 529 college savings accounts offer two major income tax advantages:

- Earnings accumulate in the account federal-income-tax-free, and

- Withdrawals to cover qualified college costs are federal-income-tax-free.

Under a special tax-law exception, in 2020, you can make a lump-sum gift of up to $75,000 to fund a Sec. 529 account set up for a child, grandchild or any other college-bound individual and claim a federal gift tax exclusion for the full amount. This is five years’ worth of the standard $15,000 exclusion that normally applies to 2020 gifts. Taking advantage of this favorable gift tax rule allows you to quickly fund a Sec. 529 college account without using up any of your unified federal gift and estate tax exemption.

If you’re married, your spouse can also use the favorable gift tax rule to make a separate 2020 gift of up to $75,000 to fund a Sec. 529 account for a child without any federal gift or estate tax consequences.

5. Pay Your Loved One’s College Tuition or Medical Bills

Under current law, you can give away unlimited amounts for the following expenses for your friends and relatives — without any federal tax consequences:

- College tuition expenses (but not room and board costs), or

- Qualified medical expenses.

There’s one hitch: You must make payments directly to the college or medical service provider.

6. Purchase Life Insurance

There’s generally no federal income tax hit on life insurance death benefits — so it can be a simple, but effective, way to transfer wealth to heirs. In other words, the beneficiaries of an insurance policy on your life will receive death benefit payments free from any federal income tax. This strategy can work equally well for unmarried and married individuals, and for beneficiaries who are family members or are unrelated.

Important: The death benefit from a policy on the life of a married person can be left to the surviving spouse without any federal estate tax hit, thanks to the unlimited marital deduction privilege (assuming the surviving spouse is a U.S. citizen). However, single people with significant net worth should beware of a potential pitfall: The death benefit from any policy on your own life is included in your estate for federal estate tax purposes if you have so-called “incidents of ownership” in the policy. It makes no difference if all the insurance money goes straight to your designated beneficiaries.

It doesn’t take much to have incidents of ownership. For example, you have incidents of ownership if you have the power to:

- Change beneficiaries,

- Borrow against the policy,

- Cancel the policy, or

- Select payment options.

This unfavorable life insurance ownership rule can expose unsuspecting high net worth individuals to the federal estate tax. To avoid this pitfall, unmarried people with large estates can set up irrevocable life insurance trusts to own policies on their lives. The death benefits can then be used to cover part or all of the estate tax bill. Your tax advisor can explain the details, including potential pitfalls, of using this strategy.

What’s Right for Your Estate?

Taxpayers can no longer count on using the stretch IRA strategy in their estate plans. But there are still other viable estate planning options available under current law. Contact your tax advisor to devise a tax-smart, up-to-date plan to transfer wealth to your loved ones.

Copyright © 2020