These days, anyone looking to form a new business relationship — especially one that involves credit — is wise to check out the risk involved first. After all, we know that even giant companies that once seemed untouchable, like Lehman Brothers and General Motors, may be teetering on too narrow a pedestal.

With that in mind, various parties might be checking out your company’s credit rating to determine whether they want to do business with you. That’s why, just as with your personal credit report, you need to be on top of what is in your business credit file.

If your company is in good standing, is free of legal hassles and has a good reputation, your credit file has the power to work for you. A good business credit score can:

- Lead to lower financing costs on loans and credit cards.

- Enable you to qualify for better credit terms from suppliers.

- Lower your insurance premiums.

Of course, this pendulum swings both ways. Negative information, even if it’s false, can leave your company with higher interest rates, lower credit limits and elevated insurance premiums, plus a loss of revenue if customers decide not to take a chance doing business with you.

What Factors Are Included?

Information in a business credit report is gleaned from a wide variety of public and private sources, including:

- The Yellow Pages and other print directories;

- Contracts and loans connected to the federal government; people and companies you’ve done business with;

- Corporate financial reports;

- Legal filings;

- Mining from Internet sites; and

- The news media.

Credit agencies like Dunn and Bradstreet (D&B) are also available to do direct investigation by request.

Does Every Business Have a Credit Score?

No. Many small businesses are judged by the personal credit score of the owner. That often happens when a sole proprietor pays business bills out of a personal checking account. Since business credit reporting agencies do gather information from sources like the Yellow Pages, there might be a bare bones record. And, if there are any recent legal judgments or pending lawsuits, these may show up and raise red flags for anyone who inquires about your business.

How Do You Find Out if Your Company Has a Business Credit File?

Pick up the phone, call Dunn and Bradstreet or Experian, or another agency that deals in business credit reporting and ask. It’s that simple.

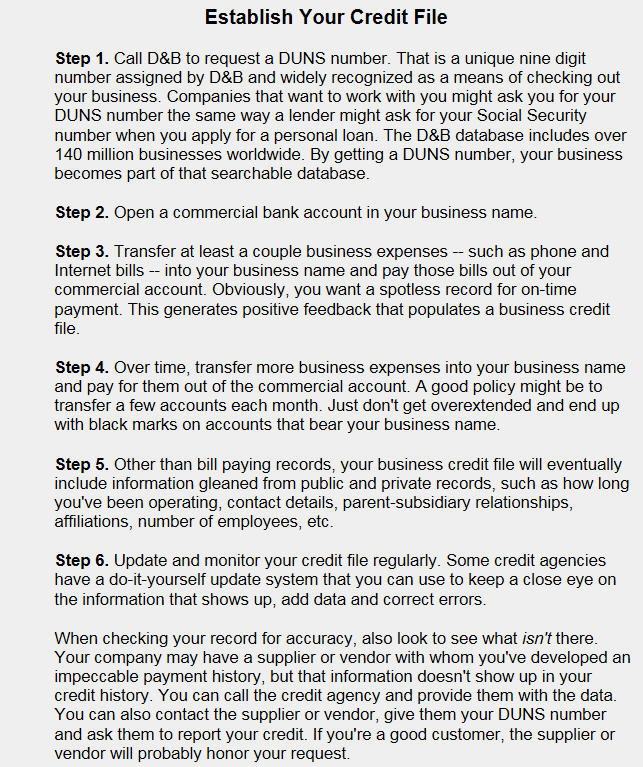

Suppose you find out that your company doesn’t have a credit file. Here’s a checklist from Dunn and Bradstreet to help you get started.

What if You Discover That Your Business Has a Bad Reputation?

Even if the negative information is inaccurate, it can keep others from doing business with you. That’s why periodic monitoring of your credit file entries is vital. If you find inaccuracies, call the credit agency and provide correct information. Negative entries that are more than two years old probably won’t show up on your business credit report.

Just as with personal credit, the most important thing to get back on track is to pay bills on time. So beware of overextending your business commitments. Get, and keep, payments into the manageable category. If the problem is cash flow, get it under control by vetting credit customers more thoroughly. Use the same credit reporting agency that others use to check out your business when deciding whether or not to extend credit.

Copyright 2016