When unused flexible spending account (FSA) balances are forfeited back to employers under the “use-it-or-lose-it” rule, employers have several options for what they can do with the money. Here is what employers need to know after first covering some necessary background information.

Flexible Spending Account Basics

Under an employer-sponsored flexible spending account (FSA) plan, employees can elect to contribute a designated amount of their annual salary to their personal health care FSA or dependent-care FSA or both.

For a health care FSA, the maximum amount that an employee can contribute for the 2020 tax year is $2,750 (up from $2,700 in 2019).

For a dependent-care FSA, the maximum amount that can be contributed is $5,000 (latest figure available). For a married employee, the $5,000 cap represents the maximum amount that both spouses can together contribute.

Employee annual FSA contribution amounts are withheld in installments from their paychecks. Employees can then use their FSA money to cover qualifying out-of-pocket medical expenses (such as amounts paid to satisfy health insurance deductibles and co-pays and amounts paid for prescription drugs, dental care and vision care) and qualifying out-of-pocket dependent-care expenses. The amounts withheld from employee paychecks are treated as a salary reduction for federal income tax, Social Security tax and Medicare tax purposes (and usually for state income tax purposes too). Reimbursements from FSAs to cover qualified out-of-pocket expenses are tax-free to employees.

To put it another way, the FSA arrangement allows participating employees to pay for all or a portion of their out-of-pocket medical expenses and dependent care expenses with pretax dollars. That is the same as getting an income tax deduction combined with a reduction in Social Security and Medicare tax withholding. The employee’s tax savings are permanent — not just a timing difference.

The Use-It-Or-Lose-It Rule

For employees, the main downside to an FSA is the use-it-or-lose-it rule. If the employee fails to incur enough qualified expenses to drain his or her FSA each year, any leftover balance generally reverts back to the employer. However, there are two exceptions to the use-it-or-lose-it rule.

- An FSA plan can allow a grace period of up to 2 1/2 months. For a calendar-year FSA plan, that gives employees up to March 15 of the following year to incur enough expenses to soak up their unused FSA balances from the previous year. (Most FSA plans are operated on a calendar-year basis.)

- A health care FSA plan can allow employees to carry over up to $500 of unused balances from one year to the next. However, if the $500 carryover privilege is allowed, the health care FSA cannot also offer the grace-period deal. In other words, a health care FSA plan can offer either the carryover privilege or the grace-period deal, but not both.

- Dependent-care FSAs cannot allow the carryover privilege, but they can allow the grace period.

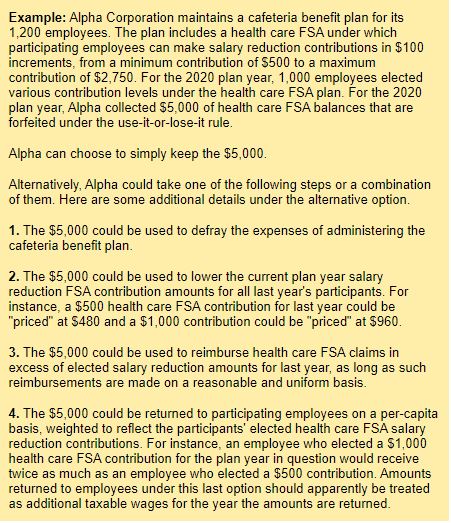

Employer Options for Forfeited FSA Balances

The IRS gives employers the following options for unused employee FSA balances that are forfeited under the use-it-or-lose-it rule. The source for this is Treasury Proposed Regulation 1.125-5(o).

1. The employer can simply keep the money.

2. If the employer doesn’t keep the money, forfeited amounts must be used for the following purposes:

- To defray expenses of administering the cafeteria benefit plan under which the FSA program or programs are offered.

- To reduce employee FSA salary reduction amounts (or employee contributions) for the immediately following FSA plan year on a reasonable and uniform basis.

- Return them to employees on a reasonable and uniform basis.

Copyright © 2020