March 2017

THE MONTH IN BRIEF

February was a great month for stocks and a historic month for the Dow Jones Industrial Average. The blue chips closed at record highs for 12 straight trading sessions, a feat unmatched for 30 years. The S&P 500 gained 3.72% for the month. Readings on consumer confidence and purchasing manager indices remained impressive, and a key home price index hit a 30-month high. The latest Consumer Price Index showed mounting inflation pressure, and the Federal Reserve hinted at an oncoming rate move.

DOMESTIC ECONOMIC HEALTH

In January, inflation spiked to a degree unseen in nearly five years as the Consumer and Producer Price Indexes both rose 0.6%. The CPI’s monthly gain was its largest since March 2012, and the PPI’s advance was its greatest since September 2012. Yearly consumer inflation reached 2.5%, a 4-year peak; annualized wholesale inflation rose to 1.6%.

It was little wonder, then, that the Federal Reserve considered the possibility of another rate hike. Minutes from its January 31-February 1 meeting revealed that “many participants” in the Federal Open Market Committee felt a quarter-point move might be warranted “fairly soon” if the labor market showed further strength and inflation pressure held. Would March be too early for an interest rate adjustment? After the minutes were released, market expectations put the chance of a March move at less than 25%, but that jumped to 50% by the end of the month.

Both purchasing manager indices maintained by the Institute for Supply Management were above the 55 level in January: ISM’s factory gauge improved 1.5 points to 56.0, and its services index ticked down but a tenth of a point to 56.5. Factory orders were up 1.3% for January, partly countering December’s 2.3% fall. The first month of 2017 also saw a 1.8% gain in hard goods orders. Industrial output tapered off by 0.3% in January after a (revised) increase of 0.6% in December.

Hiring picked up in January as firms added 227,000 net new workers, compared with (a revised) 157,000 in December. Both the U-3 and U-6 jobless rates went north, however: the former ticked up 0.1% to 4.8%; the latter increased 0.2% to 9.4%. The average wage rose 0.1%.

Consumers remained upbeat. Analysts polled by MarketWatch projected the Conference Board’s consumer confidence index to rise to 112.0 in February, but it hit 114.8 instead (a gain of 3.2 points). As for the University of Michigan’s consumer sentiment index, it went from 98.5 at the end of January to an initial February mark of 95.7, then a final February reading of 96.3.

Households were spending freely, at least according to two critical indicators. Retail sales advanced 0.4% in January, with core retail purchases up 0.8%. Personal spending had risen 0.5% in December; personal incomes, 0.3%. January figures had yet to be released as February ended. Meanwhile, the Bureau of Economic Analysis made its second estimate of Q4 growth, and the number stayed the same: 1.9%.

By executive order, President Donald Trump scheduled a review of the Dodd-Frank Act, calling for significant alterations to the financial regulations it imposed. The Trump administration seeks to improve borrowing conditions for businesses by overhauling large portions of the legislation.

GLOBAL ECONOMIC HEALTH

With the Trans-Pacific Partnership collapsing, representatives from 16 Asia-Pacific countries – including China – met in late February to discuss an alternative. The Regional Comprehensive Economic Partnership could forge an eventual trade accord between Australia, Brunei, Cambodia, China, India, Indonesia, Japan, South Korea, Laos, Malaysia, Myanmar, New Zealand, the Philippines, Singapore, Thailand, and Vietnam. Prior to last month’s RCEP talks in Kobe, Japan, Japanese Prime Minister Shinzo Abe had stated that he hoped President Trump would reconsider the U.S. withdrawal from the TPP.

New European Commission data showed that the economies of all 28 European Union member nations grew in 2016. Growth across the E.U. had not happened since 2007. The Commission forecasts inflation-adjusted economic expansion of 1.8% for the E.U. in both 2017 and 2018, and it also believes the region’s jobless rate will hit an 8-year low before 2017 ends. Euro area annualized inflation jumped 0.7% in January to 1.8%. A year earlier, yearly inflation was at just 0.3%.

WORLD MARKETS

With exceptions, February was a good month for stock benchmarks. The major exception was the Russian Micex, which sank 10.16%. Japan’s Nikkei 225 gave back 1.79%; Canada’s TSX Composite, 1.13%; and Mexico’s Bolsa, 1.19%.

Now, the gains. Brazil’s Bovespa rose 1.25%; the United Kingdom’s FTSE 100, 1.10%; the FTSE Eurofirst 300, 0.82%; France’s CAC 40, 0.38%; Spain’s IBEX 35, 0.54%; and Germany’s DAX, 0.17%. Hong Kong’s Hang Seng gained 1.63%; China’s Shanghai Composite, 2.64%; The South Korean KOSPI added 0.39%; the Indian Sensex, 3.09%. MSCI’s World Index went north 2.58% for the month, while its Emerging Markets index climbed 2.99%.

COMMODITIES MARKETS

Oil ended February at precisely $54.00 on the NYMEX, rising 2.27% during the month. Gold gained 3.15%, concluding February at a COMEX price of $1,248.80. Beyond oil and gold, some other marquee commodities advanced nicely.

Finishing February at $18.30, silver improved 4.21%. The price of platinum rose 3.22%; although, the value of copper slipped 0.48%. Heating oil futures added 1.60%; unleaded gasoline, a striking 12.52%. Natural gas futures plummeted 11.59%. Corn futures rose 1.60%, but soybeans (-0.83%), wheat (-0.77%), coffee (-6.65%), sugar (-6.41%), and cocoa (-3.59%) were among the ag losers.

REAL ESTATE

Prices were rising. Supply was tight. Who expected the pace of home buying to pick up in January? It did, though. The National Association of Realtors said that existing home sales rose 3.3%, while Census Bureau data pointed out a 3.7% advance for new home sales. The 12-month numbers were also strong: new home sales, +5.5%; resales, +3.8%. Demand simply overcame other factors. The latest S&P/Case-Shiller home price index (December) affirmed that this winter was a good time to sell: home values had risen 5.8% across the country’s 20 largest cities during 2016, taking the index to a two-and-a-half-year peak.

In contrast, pending home sales fell off in the first month of the year – the NAR reported a 2.8% drop. Mortgage rates descended a bit during February: the average interest on a conventional home loan declined 0.03% to 4.16% between January 26 and February 23, according to Freddie Mac. Freddie’s Primary Mortgage Market Survey showed similar small retreats for average interest rates on 15-year FRMs (down 0.03% to 3.37%) and 5/1-year ARMs (down 0.04% to 3.16%).

As for construction activity, the Census Bureau said that housing starts slipped 2.6% for January after December’s 11.3% gain; building permits rose 4.6%, complementing their 1.3% advance a month earlier.

LOOKING BACK…LOOKING FORWARD

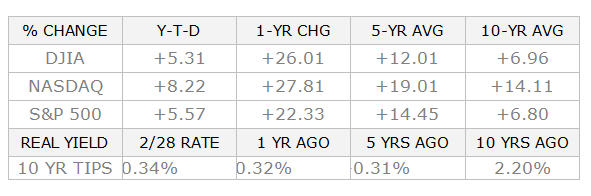

As the S&P 500 advanced 3.72% last month, the Dow Industrials gained 4.77%, and the Nasdaq Composite, 3.75%. Their respective February 28 closes: S&P, 2,363.64; Dow, 20,812.24; Nasdaq, 5,825.44. February was also a solid month for the small caps – the Russell 2000 added 1.83% to go up 2.18% on the year, finishing out the month at 1,386.68. The CBOE VIX rose 7.76% on the month to a February 28 settlement of 12.92; that still left it down 7.98% YTD.

Sources: wsj.com, bigcharts.com, treasury.gov – 2/28/17 1,2,18,19,20

Indices are unmanaged, do not incur fees or expenses, and cannot be invested into directly. These returns do not include dividends. 10-year TIPS real yield = projected return at maturity given expected inflation.

Some analysts look at the current rally in terms of irrational exuberance, while others wonder if the next phase of a historic mega-bull might be unfolding. The market will cool off at some point, that we know. Will we see that point in March? Wall Street’s confidence is such that it could probably take a quarter-point rate hike in stride this month, should one happen. So far in 2017, investors haven’t been ruffled by much – not the disconnect between a stock market at record highs and 2% economic growth, not the P/E ratio of 21 on the Dow as February ended. Will their confidence send the blue chips even higher this month? March promises to be interesting and, perhaps, historic.

UPCOMING ECONOMIC RELEASES: The roll call of major scheduled items for the rest of March starts with February factory orders (3/6) and then includes February’s ADP payrolls report (3/8), the February jobs report from the Department of Labor (3/10), the February PPI (3/14), a Federal Reserve policy decision, the February CPI and February retail sales figures (3/15), the Census Bureau’s latest data on groundbreaking and building permits (3/16), the initial March University of Michigan consumer sentiment index and February industrial output (3/17), February existing home sales (3/22), February new home sales (3/23), February hard goods orders (3/24), the March Conference Board consumer confidence index (3/28), February pending home sales (3/29), the third estimate of Q4 GDP (3/30), and the final March University of Michigan consumer sentiment index, the February PCE price index, and data on February personal income and personal spending (3/31).

Securities offered through 1st Global Capital Corp., Member FINRA/SIPC. Investment advisory services including fee-based asset management accounts held through NFS, LLC are offered through 1st Global Advisors, Inc. All other financial planning and fixed insurance services are offered through Mueller Financial Services, Inc. Mueller Financial Services, Inc. and 1st Global Capital Corp are unaffiliated entities.