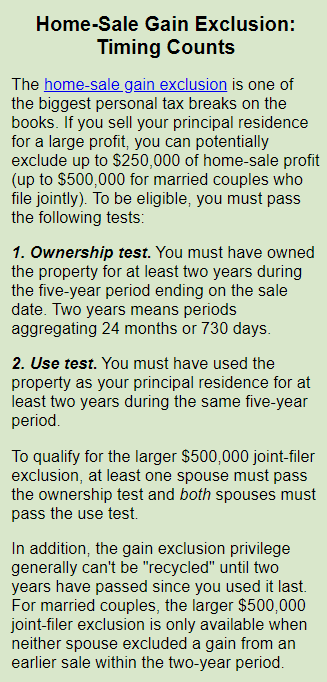

Before you sell your home, consider the tax consequences. There are some subtle nuances to the home-sale gain exclusion. (See “Home-Sale Gain Exclusion: Timing Counts” at right.) Here are some scenarios that you could fall into — and tips to help you maximize the tax-saving gain exclusion break.

Married Couples Who File Jointly with One Home

To qualify for the larger $500,000 joint-filer gain exclusion, at least one spouse must pass the ownership test and both spouses must pass the use test. When only one spouse passes both tests, the maximum gain exclusion is only $250,000.

For example, Joan and Bob got married in 2020 and immediately sold the home that Joan had owned and used as her principal residence for many years. Her gain on the 2020 sale was $600,000. The newlyweds filed a joint return for the year of sale. Unfortunately, they didn’t qualify for the $500,000 joint-filer exclusion, because Bob didn’t pass the use test. Therefore, they reported a $350,000 taxable gain ($600,000 profit minus the $250,000 exclusion) on their 2020 return. (Depending on their modified adjusted gross income, they may also owe the 3.8% net investment income tax on the portion of the gain that doesn’t qualify for the exclusion.)

Instead of selling immediately, Joan and Bob could have lived in Joan’s home for at least two years after the marriage. That way, both spouses would pass the use test, and the couple would qualify for the larger $500,000 joint-filer exclusion.

Married Couples Who File Jointly With Two Homes

If you own two homes and file jointly, each spouse’s eligibility for the $250,000 exclusion is determined separately, and each spouse is considered to own each property for any period the property is actually owned by either spouse. Actual ownership doesn’t matter as long as you file jointly.

For example, Allie and Antonio have a commuter marriage and own two homes. Allie works in Denver and lives most of the time in a condo there. Antonio works in Dallas and lives most of the time in a townhouse there. In this situation, the larger $500,000 joint-filer exclusion isn’t available for either home, because both spouses must pass the use test to qualify. However, two separate $250,000 exclusions are potentially available in this situation, assuming both homes have been owned for at least two years.

As long as Allie and Antonio file jointly in the year when a home is sold, the ownership test will be passed for that home, regardless of whether the home is owned jointly or separately. That’s because, each spouse is considered to own a property for any period the property is actually owned by either spouse. So, if they sell the Denver condo, Allie would pass both the ownership test and the use test for that property. If they sell the Dallas townhouse, Antonio would pass both tests for that property.

So, on a joint return, Allie would qualify for a $250,000 exclusion if the Denver home is sold. Likewise, Antonio would qualify for a separate $250,000 exclusion if the Dallas home is sold. This would be true whether they sell both homes in the same year or in separate years.

Married Couples Who File Separate Returns

When spouses file separate returns, it gets more complicated. They can still potentially qualify for two separate $250,000 exclusions. But in the separate return scenario, actual ownership matters.

For example, if you and your spouse own a property jointly and you both live there, you can potentially exclude up to $250,000 of your share of the gain on your separate return if the property is sold. Your spouse can do the same.

Alternatively, if you and your spouse own two properties separately and live in them separately, you can potentially exclude up to $250,000 of gain on the sale of your property. Your spouse can do the same on the sale of his or her property.

Surviving Spouses

If your spouse died and you’ve not remarried, you can’t file a joint return for any year after the year in which your spouse died. Previously, this rule could have prevented you from taking advantage of the $500,000 exclusion that’s allowed to joint filers, because you would have been limited to the smaller $250,000 single-filer exclusion if you sold your home in a year after the year in which your spouse died. Congress addressed this problem but didn’t completely cure it.

Under current tax law, an unmarried surviving spouse can claim the larger $500,000 gain exclusion if the following conditions are met:

- The sale is of a principal residence,

- It occurs within two years after the spouse’s date of death, and

- All the other requirements for the $500,000 exclusion were met immediately before the spouse died.

You have to get the timing just right to qualify. Because the two-year eligibility period for the larger exclusion begins on the date of the spouse’s death, a sale that occurs in the second calendar year following the year of death, but more than 24 months after the date of death, won’t qualify for the larger $500,000 gain exclusion.

Claiming a Reduced Exclusion

What happens if you fail to pass all the timing requirements for the home-sale gain exclusion? For example, you might sell your home for a healthy profit after living there only 18 months instead of the required two years. Or you might sell your current home less than two years after excluding gain from the sale of a previous residence.

You might not be required to pay tax on the entire gain when you make such a “premature” sale. That’s because IRS regulations allow you to claim a reduced exclusion — some fraction of the full $250,000 or $500,000 amount — when you sell your home due to:

- A change of place of employment,

- Health reasons, or

- Other unforeseen circumstances, as specified by the IRS.

The reduced exclusion equals the $250,000 single-filer or $500,000 joint-filer exclusion, whichever applies, multiplied by a fraction. The numerator (top number of the fraction) is the shorter of:

- The aggregate period of time the property is owned and used as your principal residence during the five-year period ending on the sale date, or

- The period between the last sale for which you claimed an exclusion and the sale date for the home currently being sold.

The denominator (bottom number of the fraction) is two years (24 months or 730 days). To clarify, here are some examples:

Betty and Chris are married and file a joint return. Due to a job change that required a long-distance move, they sold a home that they’d owned and used as their principal residence for only 11 months. The gain on the sale was $200,000. This couple is entitled to a reduced gain exclusion of $229,167 ($500,000 x 11/24), which means their entire gain would be excluded from federal income tax.

Sam is a single taxpayer. He sold his previous home 15 months ago and claimed the gain exclusion privilege. Due to health reasons, he’s now about to close on the sale of his current home, which he’s owned and used as his principal residence for only 15 months. The gain will be $150,000. Sam is entitled to a reduced gain exclusion of $156,250 ($250,000 x 15/24), which means his entire gain would be excluded from federal income tax.

For More Information

Your tax advisor can explain the sometimes complicated home-sale gain exclusion rules and offer tips to help you maximize your tax savings. In some cases, a small difference in timing or circumstances can make a big difference in your tax situation. Contact your tax pro before you put your house on the market.

Copyright©2021